Saving for a down payment has long been one of the biggest obstacles for homebuyers…

Mortgage interest rate predictions: Will rates go down in February 2022?

Mortgage interest rate predictions: Will rates go down in February 2022?

Paul Centopani The Mortgage Reports Editor

Mortgage rates surged through the beginning of 2022 and show no signs of stopping.

After settling at a 3.05% average on December 23, 2021, 30–year fixed interest rates grew significantly in the five weeks since and averaged 3.55% on January 27, 2022 – the highest range since March 2020.

With the Federal Reserve tightening its monetary policies to offset inflation, that growth will likely continue in February.

Will mortgage rates go down in February?

Mortgage rates greatly expanded in January and indicators point to more growth for February.

Between high inflation, Fed policy changes, and the dwindling impact of Omicron, industry experts are in near–consensus that rates will rise – with high–end predictions that they could spike by as much as 100 basis points (a full percentage point) in the next few months.

Doug Duncan, Fannie Mae chief economist and senior vice president

Prediction: Rates will rise

“What precipitated this significant run up in the mortgage rates was the release of the minutes of the Fed. The market was not prepared for the statement that they would start to aggressively run the MBS portfolio off and the potential to move Fed Funds targets forward.

That started some movements in mortgage spreads. It also started some movements in rates. There are historical precedents to this. In 2013 the chair of the Federal Reserve made a speech saying it would stop buying securities at some point. Mortgage rates ran up 100 basis points in the following six months.

The Fed tightened again in the 2017–2018 time period and started raising the Fed Funds rate and running the portfolio off. Mortgage rates ran up 100 basis points over the course of a year. What we should expect is if interest rates continue to rise at the pace they are, that would suggest a rise of 100 basis points in three months.

If the Fed really does start running out its portfolio mid–year, then I think there is a reason to believe that rates rise.

Nadia Evangelou, National Association of Realtors senior economist and director of forecasting

Prediction: Rates will rise

“Mortgage rates will continue to rise in February. Inflation will remain elevated as the Fed won’t likely raise interest rates in the next couple of months.

Remember that when inflation rises, lenders demand higher interest rates as compensation for the decrease in purchasing power. Thus, I expect the 30–year fixed mortgage rate to average 3.5% in February.”

Selma Hepp, CoreLogic Deputy Chief Economist

Prediction: Rates will stay flat

Mortgage rates have already jumped about 50 bps since the beginning of the year as markets respond to Fed’s signals of upcoming lift off in rates. With Fed rate hikes already priced into yields, mortgage rates are likely to remain flat in February.

In addition, higher interest rates have not deterred home buyers or homebuilder sentiment, which is close to record levels – another reason that may keep rates where they are.

Joel Kan, Mortgage Bankers Association associate vice president of economic and industry forecasting

Prediction: Rates will rise

“Our forecast is for the 30–year fixed rate to gradually increase over the course of the year, reaching 4.0% in Q4 2022.

Another year of strong economic growth combined with the Fed’s tighter policy stance will put upward pressure on rates, and as the Fed reduces its MBS purchases, we also expect some volatility as other investors step into the market but without the steady purchase flow of the Fed.”

Odeta Kushi, First American deputy chief economist

Prediction: Rates will rise

“Multiple factors point to continued upward pressure on mortgage rates in February. The Federal Reserve has signaled that the end of the easy money era is near. Fed tightening, in combination with a growing economy, is likely to translate to a gradual rise in mortgage rates.

Of course, the pandemic remains in the driver’s seat, and any resurgence of COVID, or any other economic, market, or geopolitical shock, could result in downward pressure on rates.”

Taylor Marr, Redfin deputy chief economist

Prediction: Rates will rise

“Rates are volatile and uncertain right now, but there is a significantly higher probability that rates will still increase through February rather than decrease, albeit only slightly. Meaning, there is more risk that mortgage rates will continue slowly rising vs falling.

I expect that the mortgage rate growth in January was reflective of investors adjusting to several factors. Examples are clarity over Omicron’s economic impact (which was uncertain through December), and increased certainty over the Fed tightening monetary policy to tame inflation.

This included a runoff of Mortgage Backed Securities on their balance sheet, which simply means that the Fed will pull back demand for mortgages–lowering prices and raising market rates.

Finally, mortgage rates follow closely the yield on 10–year treasuries, which are also heavily influenced by foreign yields and central bank behavior in countries such as Japan, Canada and Germany, and nearly all are engaging in tighter monetary policy.”

Todd Teta, Attom Data Solutions chief technology and product officer

Prediction: Rates will rise

“Home–mortgage rates look like they are headed up based on recent indicators from the Federal Reserve Bank, which point toward pulling back on economic stimulus and increasing interest rates as a way to try to head off rising inflation.

If the Fed boosts rates, that will result in mortgage rates going up. How much they increase is something we are watching closely, but it seems like some kind of increase will show up by February.”

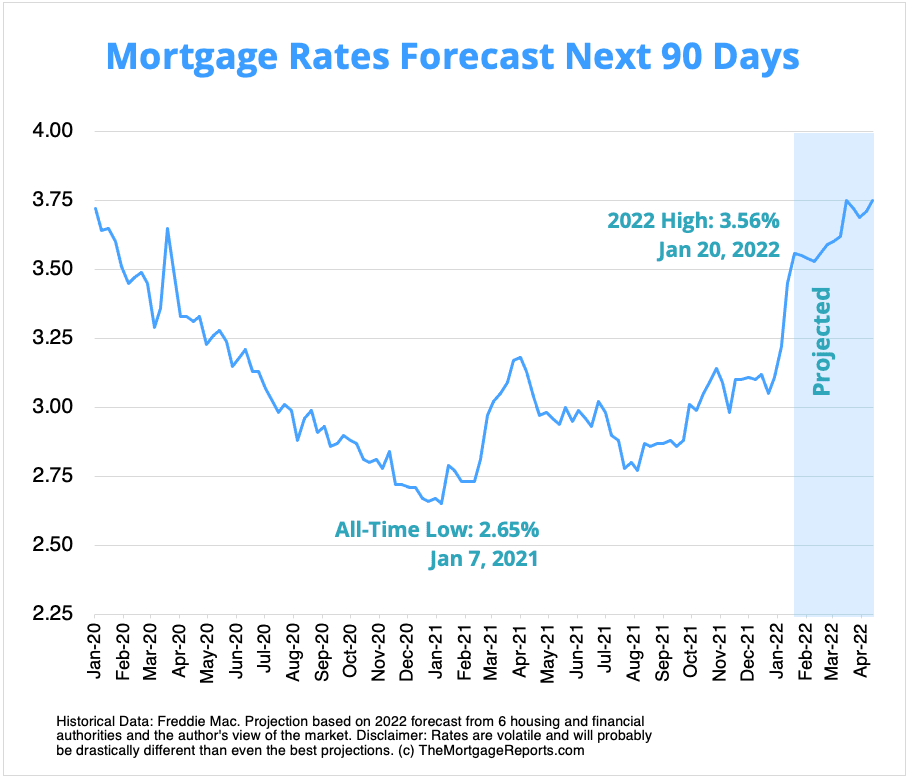

Mortgage interest rates forecast next 90 days

Barring the pandemic bringing the economy to a halt, it’s very probable mortgage rates will rise over the upcoming three months.

Of course, interest rates rarely move in a straight line and can rise or drop from one week to the next. So while the overall averages should continue to climb, it’s highly likely we see some sideways and downward movements mixed in along the way.

Mortgage rate predictions for 2022

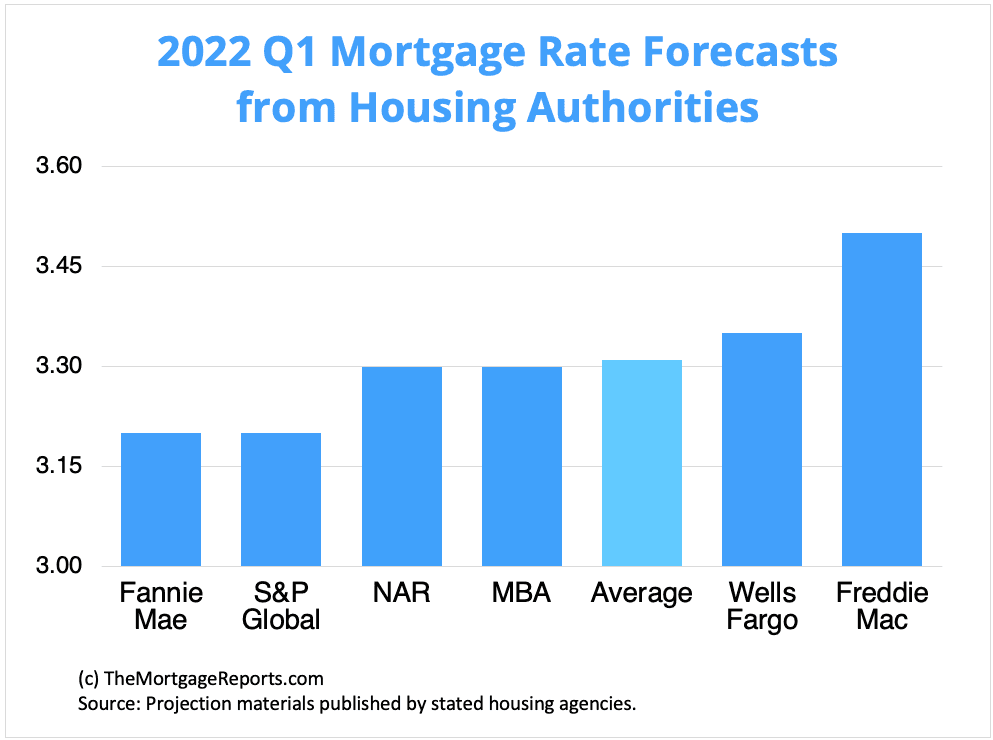

The average 30–year fixed rate mortgage ended 2021 at 3.10%, according to Freddie Mac.

All six of the major housing authorities we gathered expect that average to rise over the first quarter of 2022.

Fannie Mae and S&P Global sit at the low end of the spectrum, estimating the average 30–year fixed interest rate to settle at 3.20% by the end of Q1. Wells Fargo and Freddie Mac had the highest predictions, with forecasts of 3.35% and 3.50%, respectively, by the end of March.

Current mortgage interest rate trends

Mortgage rates went through a growth spurt to kick off 2022.

Though last week (Jan. 27) the average 30–year fixed rate slightly decreased from 3.56% to 3.55%, according to Freddie Mac’s weekly rate survey.

The past five weeks accounted for a growth of 50 basis points and saw the average climb to the highest level since 3.65% on March 19, 2020.

The 15–year fixed rates showcased similar hikes, most recently inching up from 2.79% to 2.80%, while the average rate for a 5/1 ARM jumped from 2.60% to 2.70%.

Mortgage rates are moving away from the record–low territory seen in 2020 and 2021.

But keep in mind that rates are still ultra–low from a historical perspective.

Just three years ago, in December 2018, 30–year rates averaged 4.75% according to Freddie Mac’s survey. And in December 2019 they hovered around 3.75%.

So if you haven’t locked a rate yet, don’t lose too much sleep over it. There are still great deals to be had – especially for borrowers with strong credit.

Just make sure you shop around to find the best lender and lowest rate for your unique situation.

Mortgage rate trends by loan type

Many mortgage shoppers don’t realize there are different types of rates in today’s mortgage market.

But this knowledge can help home buyers and refinancing households find the best value for their situation.

Following are 3–month mortgage rate trends for the most popular types of home loans: conventional, FHA, VA, and jumbo.

| December 2021 | November 2021 | October 2021 | |

| Conforming Loan Rates | 3.35% | 3.27% | 3.27% |

| FHA Loan Rates | 3.45% | 3.38% | 3.39% |

| VA Loan Rates | 3.02% | 2.96% | 2.96% |

| Jumbo Loan Rates | 3.23% | 3.24% | 3.19% |

Which mortgage loan is best?

The best mortgage for you depends on your financial situation and your goals.

For instance, if you want to buy a high–priced home and you have great credit, a jumbo loan is your best bet. Jumbo mortgages allow loan amounts above conforming loan limits – which max out at $647,200 in most parts of the U.S.

On the other hand, if you’re a veteran or service member, a VA loan is almost always the right choice.

VA loans are backed by the U.S. Department of Veterans Affairs. They provide ultra–low rates and never charge private mortgage insurance (PMI). But you need an eligible service history to qualify.

Conforming loans and FHA loans (those backed by the Federal Housing Administration) are great low–down–payment options.

Conforming loans allow as little as 3% down with FICO scores starting at 620.

FHA loans are even more lenient about credit; home buyers can often qualify with a score of 580 or higher, and a less–than–perfect credit history might not disqualify you.

Finally, consider a USDA loan if you want to buy or refinance real estate in a rural area. USDA loans have below–market rates – similar to VA – and reduced mortgage insurance costs. The catch? You need to live in a ‘rural’ area and have moderate or low income to be USDA–eligible.

Mortgage rate strategies for February 2022

Mortgage rates are rising – a trend that should continue in February and the rest of 2022. However, great opportunities to lock in a low interest rate still exist for home buyers and refinancing homeowners.

Here are just a few strategies to keep in mind if you’re mortgage shopping in the next few months.

Lock it up

If you missed out on getting a mortgage or refinancing while rates bottomed–out over the last two years, don’t let that hold you back.

Even though rates climbed back above 3%, they’re still historically low. Of course, nobody knows with 100% certainty where future rates will trend and we can only make the best decisions given what we do know today.

Current economic indicators signal more interest rate growth is on the way and industry experts forecast them to approach 4% by year’s end.

Taking all the necessary steps to get a mortgage is key to being prepared and locking in a rate when the right time comes for you.

Shop around

Competition drives innovation. In our case, competition drives lower interest rates.

As rates rise in 2022, the demand for refinancing (and to a certain extent, purchasing) will fall. This will lead to lenders having less in their pipelines and more of a need for new business.

Doing the legwork and connecting with a few different lenders can seem daunting at first but could help you shave percentage points off of your mortgage rate and save you money over the lifetime of your loan.

How to compare interest rates

Rate shopping doesn’t just mean looking at the lowest rates advertised online because those aren’t available to everyone. Typically, those are offered to borrowers with perfect credit and who can put a down payment of 20% or more.

The rate lenders actually offer depends on:

- Your credit score and credit history

- Your personal finances

- Your down payment (if buying a home)

- Your home equity (if refinancing)

- Your loan–to–value ratio (LTV)

- Your debt–to–income ratio (DTI)

To figure out what rate a lender can offer you based on those factors, you have to fill out a loan application. Lenders will check your credit and verify your income and debts, then give you a ‘real’ rate quote based on your financial situation.

You should get 3–5 of these quotes at minimum. Then compare them to find the best offer.

Look for the lowest rate, but also pay attention to your annual percentage rate (APR), estimated closing costs, and ‘discount points’ – extra fees charged upfront to lower your rate.

This might sound like a lot of work. But you can easily shop mortgage rates in a day if you put your mind to it. And shaving just a few basis points off your rate can save you thousands.

Related Posts